Andy Keeler

Executive Summary: Should I Pay Off My Mortgage? Buy or Lease A Car? It’s Mind Vs. Math

In this mailbag episode, Andy Keeler is joined by Abby Rose, CFP®, CPA; Mark Beaver, CFP®; and Jake Martin, CFP®, to answer common financial questions from clients and prospects. The discussion highlights a recurring theme: many financial decisions depend on individual circumstances, tax considerations, and personal comfort levels.October 14th, 2025 | 4 min read

Executive Summary: Should I Pay Off My Mortgage? Buy or Lease A Car? It’s Mind Vs. Math

In this episode of Should I Pay Off My Mortgage? Buy or Lease A Car? It’s Mind Vs. Math: “Ever wonder why your Roth “feels” slower than your 401(k)? You’re nearing retirement and want to be mortgage free…”Key Takeaways

Financial planning decisions often look simple on the surface, but once you dig deeper, they almost always involve both math and mindset. Below are some of the most common questions we have been addressing, along with the context that is often overlooked.

Account Types vs. Investment Growth

One of the biggest areas of confusion involves the difference between account types such as Roth IRA, Traditional IRA, brokerage, or 401(k) and the investments inside them. Growth is driven by what you are invested in, not the label on the account.

Balances can look dramatically different because of:

- Contribution amounts

- Employer matching

- Years invested

- Tax treatment

Without understanding those variables, it is easy to make inaccurate comparisons.

Roth vs. Pre-Tax 401(k)

The Roth versus pre-tax decision primarily depends on your current tax bracket compared to your expected future tax bracket.

General guidelines include:

- Lower brackets (10 to 12 percent): Roth contributions often make sense.

- Higher brackets (32 percent and above): Pre-tax contributions may be more advantageous.

- Middle brackets (22 to 24 percent): Requires deeper analysis and often a blended strategy.

It is also important to note that certain high earners are now required to make catch-up contributions to a Roth if their income exceeded $150,000 in the prior year. That rule alone can significantly influence planning decisions.

FAFSA Timing and Strategy

Although the federal FAFSA deadline extends well into the academic year, families should file as early as possible.

Reasons to file early:

- Many state and institutional aid programs operate on a first-come, first-served basis.

- Filing early can improve access to limited funds.

- The process is now streamlined with IRS data integration.

Waiting may unintentionally reduce financial aid opportunities.

Paying Off a Mortgage Before Retirement

From a purely financial standpoint, keeping a low-interest mortgage while investing excess cash often produces stronger long-term results.

However, this decision is not strictly mathematical.

Being debt-free can:

- Reduce stress

- Increase retirement confidence

- Improve cash flow flexibility

The emotional value of eliminating debt must be weighed alongside potential investment returns.

Investing in Gold

Gold is often discussed as an inflation hedge or a “fear asset.” While it has performed well in recent years, long-term inflation-adjusted returns have historically been inconsistent.

Gold may serve as:

- A limited portfolio diversifier

- A hedge during periods of uncertainty

However, it also carries volatility and has experienced long periods of flat performance. It is rarely a primary growth solution.

Long-Term Care Insurance

Today’s hybrid life insurance and long-term care policies offer more flexibility than traditional “use-it-or-lose-it” plans.

Suitability depends on:

- Asset levels

- Ability to self-fund care

- Family health history

- Desire for peace of mind

In many cases, the psychological relief of having coverage is just as important as the financial protection itself.

529 Plans vs. Brokerage Accounts

For families saving for education, 529 plans remain highly advantageous due to tax-free growth and expanding flexibility.

Key advantages include:

- Tax-free qualified withdrawals

- Potential state tax deductions

- K–12 usage options

- Limited Roth IRA rollover flexibility

While investment choices may be narrower and non-qualified withdrawals carry penalties, 529 plans generally provide superior long-term efficiency for education savings.

Leasing vs. Buying a Car

This decision depends on driving habits, cash flow, lifestyle preferences, market conditions, and long-term ownership goals.

Leasing can provide:

- Predictable monthly payments

- Lower short-term cash outlay

- Regular vehicle upgrades

Buying, especially slightly used, may:

- Reduce long-term ownership costs

- Eliminate recurring payments

- Provide greater long-term value

There is no universal answer. The right choice depends on personal priorities.

The Bigger Picture

Nearly every financial decision has both a quantitative component and a psychological component.

Sound planning balances tax efficiency, risk management, long-term outcomes, and personal peace of mind. The goal is not just optimization. It is alignment.

The opinions expressed in this program are for general informational purposes only and are not intended to provide specific advice or recommendations.

It is only intended to provide education about finance, tax, retirement and related planning topics. To determine which investments or strategies may be appropriate for you, consult your financial, tax or legal advisor prior to implementing. Any past performance discussed during this program is no guarantee of future results.

Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Keeler & Nadler Family Wealth is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Keeler & Nadler Family Wealth and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Keeler & Nadler Family Wealth unless a client service agreement is in place.

More Recent Blogs

Smart money tips & life planning advice

Laid Off in Your 50s or 60s? Here Is Your Financial Survival Guide

Prepare your child for college with this financial checklist for high-net-worth families. From legal protections to tuition planning, ensure a secure transition. This carefully organized checklist highlights the critical areas to focus on, from legal healthcare protections and financial readiness to tuition planning and insurance considerations.

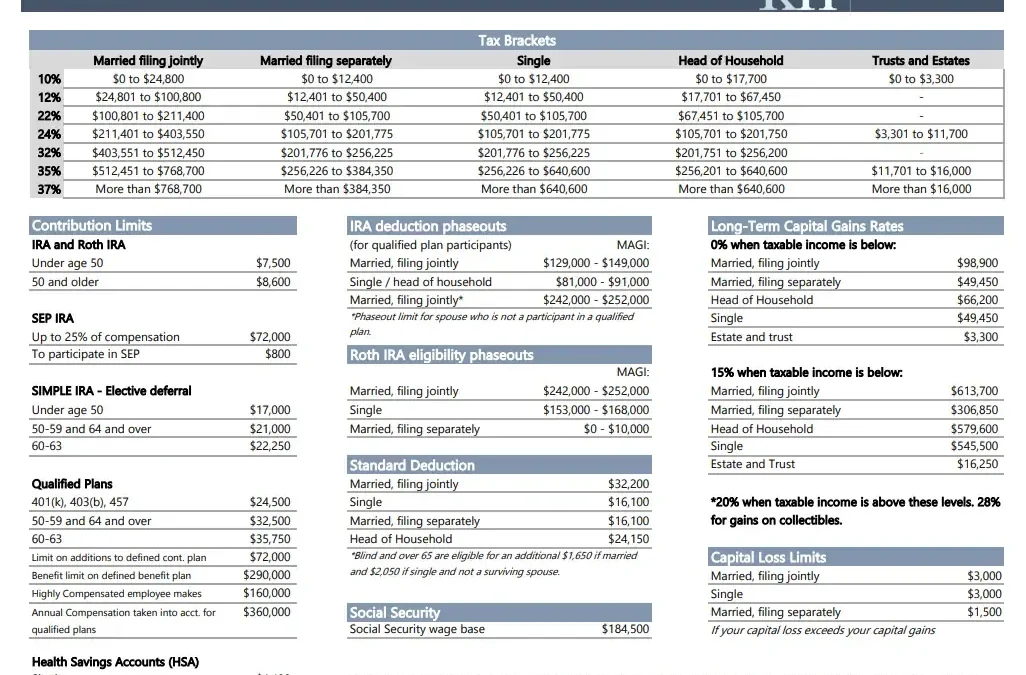

2026 Tax Guide: Key Tax Updates & Planning Considerations

Mark BeaverThe Keeler & Nadler Family Wealth 2026 Tax Guide is now available. Each year, tax law updates create new planning opportunities and potential pitfalls for individuals, families, and business owners. Our latest guide highlights the most important changes...

The Blind Spots That Cost DIY Investors Thousands

Discover why even savvy DIY investors—doctors, lawyers, and executives—turn to KN Family Wealth for tax planning, retirement strategies, and peace of mind. Listen now on the Keeler & Nadler Podcast.